Warsh’s first FOMC meeting will put policy and Fed independence in focus

- 06.12.26

- Markets & Investing

- Commentary

Review the latest Weekly Headings by CIO Larry Adam.

Key takeaways:

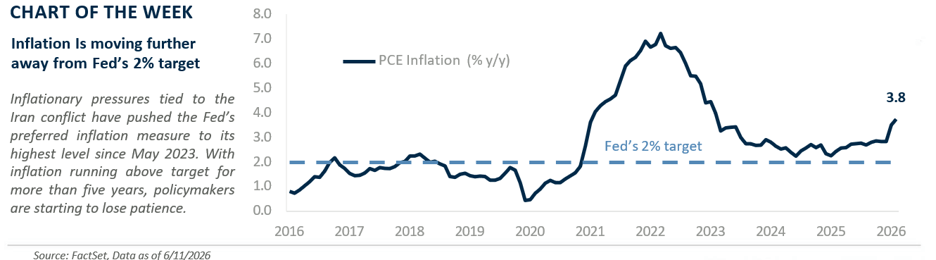

- Inflation has been above the Fed’s 2.0% for over five straight years

- The Fed’s dot plot is likely to signal no rate cuts in 2026

- Fed independence will be an early test for Warsh

New Federal Reserve Chairman Kevin Warsh will preside over his first Federal Open Market Committee (FOMC) meeting on June 16-17, stepping in at a complex moment with inflation at a three-year high as oil prices remain elevated, labor market risks easing with job growth averaging ~140,000 year to date versus only 10,000 last year, and hawkish voices on the Fed gaining traction.

Policymakers are still expected to hold rates steady as they assess next steps. While quarterly meetings typically carry added weight given the updated Summary of Economic Projections (SEP) and the dot plot, this one stands out even more. Markets have yet to gauge Warsh’s communication style, raising the stakes. How he delivers the decision in his first post-meeting press conference, signals policy into year-end and 2027, and addresses Fed independence will help define his tenure. Below, we outline what to watch and our updated Fed views.

The Kevin Warsh era begins

Warsh steps in at a challenging moment: Inflation is running nearly 2% above target, the labor market is gradually firming, and markets are pricing in nearly one rate hike by year-end. He brings a clear vision, favoring less frequent communication, renewed focus on the Fed’s core mandate – price stability and full employment – and reduced reliance on non-traditional tools like balance sheet expansion (for example, quantitative easing).

At the margin, he may introduce modest changes, such as scaling back post-meeting press conferences, though broader shifts will take time. For now, markets are focused on his communication style, how he shapes the policy statement and signals his approach to leading the Fed. Also worth watching is the role Jerome Powell takes on, as he remains at the Fed after his term as chairman ended, the first time that’s happened in approximately 80 years.

Updated projections still coming

While Warsh has been critical of the Fed’s forward guidance, an updated Summary of Economic Projections will still accompany the June meeting. Markets will be focused on any shifts in the Fed’s growth, inflation and rate outlook. In March, the dot plot pointed to one cut in 2026 and another in 2027, but the case for easing this year has faded.

Growth remains resilient – supported by fiscal tailwinds and strong business investment – and the labor market continues to firm, with three-month average job gains of +188,000, the fastest since March 2024. Inflation, however, remains the key concern. After raising its year-end core PCE forecast to 2.7% in March, another upward revision in the SEP looks likely. We also expect the Fed to drop its easing bias and no longer signal a 2026 rate cut, in line with our view. We’ll also be watching closely for any shift in the median longer-run neutral rate – a level that neither supports nor restricts economic growth – currently estimated at 3.1%.

Fed independence to endure

Fed independence will be an early test for Warsh. While he pledged to keep policy independent during his Congressional testimony, some market skepticism remains about whether political pressure, particularly from President Trump, or his evolving policy lean could blur that line.

With the macro backdrop no longer supportive of rate cuts, Warsh has an opportunity to establish credibility and create distance from the White House. Notably, President Trump even urged him to be “totally independent” and “just do your own thing” at his swearing-in, underscoring the spotlight on this issue. For now, markets remain focused on the near-term rate path, but the Fed’s institutional guardrails are firmly in place. By design, the chair is just one of twelve voting members – seven governors and five regional Fed presidents – with influence driven by consensus-building, not authority. One person, one vote. Legal challenges have also reaffirmed the Fed’s unique independence. If anything, recent tests have strengthened, not weakened, the institution.

No rate cut in 2026, but 2027 still in play

Heading into 2026, we expected the Fed to retain an easing bias, with one additional rate cut late in the year. That below-consensus view – markets were pricing in two or more cuts – was based on a softer labor market and continued disinflation. But both have shifted. The labor market has firmed, with jobless claims near multi-decade lows, hiring stabilizing, and unemployment at 4.3%. At the same time, the Iran conflict has pushed inflation to multi-year highs, and forward-looking indicators – PPI and ISM price components – point to renewed pressure.

As a result, we no longer expect a rate cut in 2026. Does that mean the next move is a hike? We don’t think so. Markets are pricing in nearly two hikes over the next 12 months, which we see as too aggressive. A de-escalation in the US-Iran conflict should ease energy prices – our year-end forecast is ~$70 to $75 per barrel – allowing disinflation to reassert itself. Longer term, AI-driven productivity, technological gains, and moderated wage growth (~3.4% year over year) should help contain inflation, setting the stage for the Fed to resume easing in 2027.

The takeaway: The easing cycle is delayed, not derailed, supporting growth, anchoring rates and providing a constructive backdrop for earnings and equities.

*MAGMAN represents a composite of Microsoft, Apple, Google, Meta, Amazon, Nvidia.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.