With major economic data delayed, corporate earnings take center stage

- 10.17.25

- Markets & Investing

- Commentary

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- With official data delayed, corporate commentary is especially useful

- AI demand and consumer resilience remain key themes domestically

- On the international front, companies will shed light on forex and tariffs

It’s that time of year again! The calendar has turned to a period when market attention shifts from the big-picture macro trends—interest rates, inflation, tariffs, and labor dynamics—to the micro details, as the S&P 500’s third-quarter earnings season moves into full swing. This time, earnings reports carry even greater significance. With major economic data delayed due to the ongoing government shutdown, investors are relying more heavily on company disclosures to gauge the health of the economy. In the absence of official government statistics, earnings calls and management commentary will serve as critical sources of insight into current conditions and future expectations. Uncertainty remains elevated, and the coming weeks will be shaped by the signals embedded in these reports. Below are five thematic areas we will be monitoring closely, each offering important clues about where the economy and markets may be headed.

- How Are Consumers Holding Up? | Recent signs of a softer job market and tariff pressures have raised concerns about consumer strength, especially among lower-income households. This is showing up in earnings forecasts for Consumer Discretionary and Staples—two of the four sectors expected to post EPS declines in 3Q. The ~2% drop projected for Consumer Discretionary would be its first YoY decline since 4Q22. Key questions to watch: Will tariffs further weigh on goods spending or crimp retailer margins? Are shoppers trading down to value retailers like Walmart and dollar stores? So far, early reports point to resilience: major banks see solid debit and credit card trends, airlines report strong travel demand, and luxury leader LVMH posted its best U.S. sales growth since 2023. Still, we expect tariffs and slower hiring to pressure spending ahead—particularly for lower-income households—so we remain cautious on consumer-focused sectors.

- Can Tech Keep Leading the Pack? | Tech has dominated earnings in recent quarters. Since 2022, full-year earnings for the MAGMAN* group have jumped 140%, versus just 7% for the rest of the index. With talk of a tech bubble growing, 3Q results will be key to gauging the health of AI and tech investment. Current 3Q estimates call for MAGMAN earnings to rise 18%, marking the 11th straight quarter of outperformance versus the rest of the index (current estimate: just +4%). Early overseas reports from ASML and TSMC suggest the AI supply chain remains strong. Still, guidance from software firms and data center giants will be critical for spotting future trends. Looking ahead, the Tech sector is expected to beat the S&P 500 each quarter through 2026, with margins roughly double (27% vs. 13%) and shareholder-friendly actions (increased dividends and buybacks) remaining supportive. We remain overweight the tech sector.

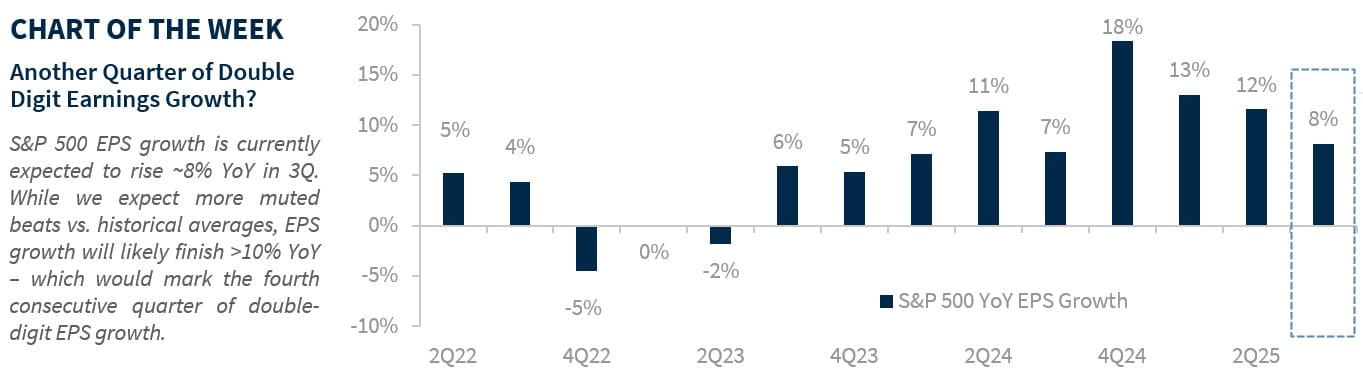

- Can Earnings Surpass A Higher Bar? | Companies face tougher expectations heading into this earnings season. Over the past 12 weeks, S&P 500 earnings estimates have ticked up 0.4%, compared to an average 3.2% cut over the last decade. Strong economic growth (Atlanta Fed GDPNow: +3.9%) should support more beats in 3Q, though these beats may be smaller than recent quarters (10-quarter average: +6.8%). However, we still expect the S&P 500 to notch its fourth consecutive quarter of double-digit earnings growth. Investors will likely focus more on top-line revenue growth than cost-cutting measures like layoffs. With valuations elevated, misses could be punished sharply—last quarter, companies that fell short lagged the broader market by 5.8% the next day by the widest margin since 2017.

- How Are Companies Managing Tariff Impact? | New country-level tariffs took effect on August 7, so 3Q results may only show a partial impact—and it will vary by company and sector. For many, the full effect may not hit until 4Q or even early 2026, depending on supply chains. Sectors with strong pricing power, like Technology and Health Care, are most likely to pass costs through. By contrast, areas like Materials and Consumer Staples, where products are more commoditized, may have less flexibility and cause further compression in their margins. Even if tariffs don’t show up in this quarter’s numbers or guidance, expect conference calls to focus on how firms plan to respond—whether through price hikes, sourcing changes, or other strategies.

- Will Small-Caps Earnings Support a Further Breakout? | Small-cap stocks (Russell 2000) have surprisingly been outperforming large caps (S&P 500) since the April bottom—but their earnings tell a different story. The level of small-cap earnings are still 7% below its 2021 peak, while large-cap earnings are up 22% over the same period. Heading into 3Q, expectations are optimistic: small-cap EPS is projected to rise ~7%, marking only the third quarter of growth in three years. Full-year estimates have finally stabilized and are inching higher, but risks remain. Heavy exposure to regional banks (with potential write-downs as credit concerns linger) and unprofitable tech could weigh on results. With fundamentals still stronger for large caps, we continue to favor them over small caps.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.