A short note on the US Supreme Court’s decision on tariffs

- 02.20.26

- Economy & Policy

- Commentary

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

We will let lawyers determine the path forward on tariffs after the Supreme Court’s decision, but we want to give our two cents from inside our economist castle tower. As we have said before, we believe that freer trade is better than no trade, and tariffs are not good instruments to solve economic problems. However, this has nothing to do with today’s Supreme Court decision deeming the International Emergency Economic Powers Act (IEEPA) tariffs illegal. The administration will have other alternatives to impose tariffs on a sector-by-sector basis, or it could potentially accept the decision and say that its objectives were achieved and move forward. We don’t really know what it will do, but we suspect it will try to come back and impose other tariffs.

The biggest issue we have with this is the uncertainty it creates and economic distortions we are going to see going forward. We could once again see firms trying to hoard imports in order to avoid sectoral tariffs, potentially generating even more uncertainty. We already saw what happened after the April 2 Liberation Day shock, and the employment data after revisions clearly showed the negative effects on US firms. Thus, we are concerned that the decision to reimpose tariffs and the resulting uncertainty could delay the recovery in employment we were expecting. Hard to say right now, but we will follow these events closely during the next several quarters.

Hard versus soft data: The winner is… soft data

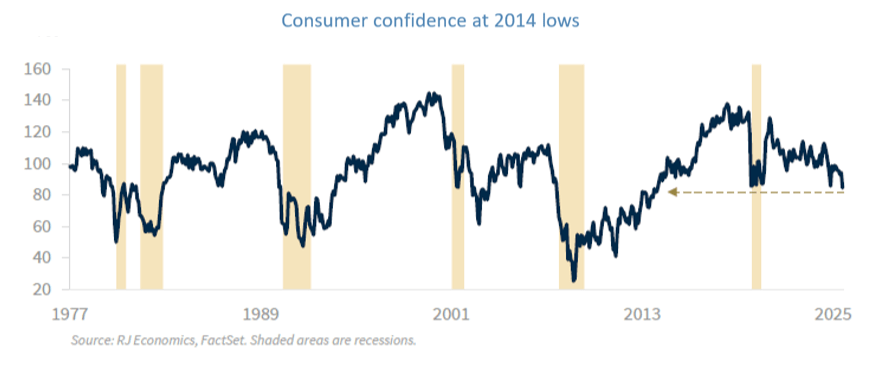

During 2025, there was a big discussion around the discrepancy between hard data, which continued to point to a very resilient US economy, and consumers’ responses in surveys (soft data) about how they felt regarding the economy. The relatively large jump in consumer confidence after the November 2024 presidential election was short-lived, with the Consumer Confidence Index (CCI) dropping back to levels not seen since 2014, mostly due to the impact of Liberation Day in April of last year. Although we saw some recovery in the aftermath, the index started to fall again in August 2025 and reached the lowest level since early 2014 once more in January of this year.

The consequences of the imposition of tariffs last year seem to have clouded economists’ and analysts’ views of what the first thing companies do when faced with a shock. Since early last year, we were arguing for a more forceful lowering of interest rates because we saw that employment was slowing down considerably. We had trouble convincing friends and foes because employment numbers (hard data) were pointing to a still strong labor market. However, when firms are caught by surprise by an unforeseen event, in this case a tariff shock, the only factor of production they can cut almost immediately is labor. Although we didn’t see massive layoffs that would indicate a recession, firms decided to slow down hiring even as the economy continued to grow.

At the same time, the One Big Beautiful Bill Act (OBBBA) provided a very large incentive to invest in capital rather than labor, as firms could fully expense capital investment and reduce their tax bill. This meant that the OBBBA provided incentives at a time of high uncertainty due to tariffs.

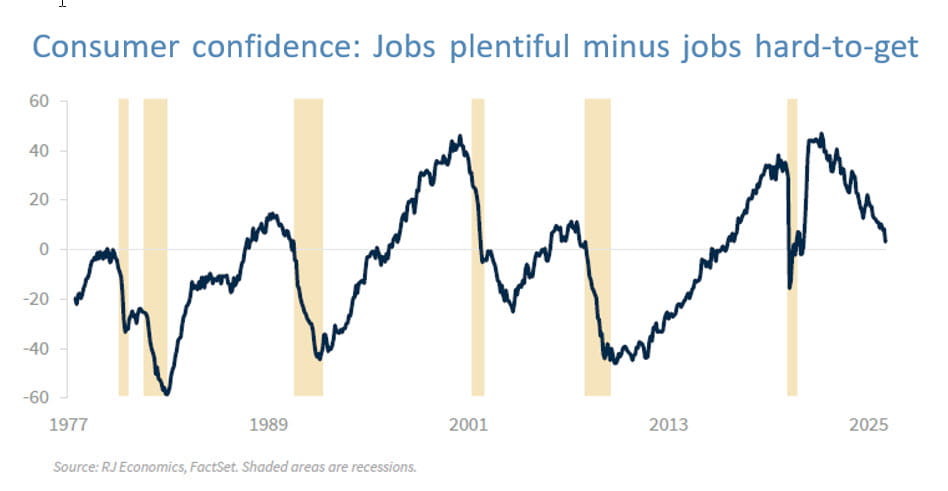

Americans have been concerned with the state of the US labor market for a while, but this concern accelerated at the beginning of 2025, with the difference between “jobs plentiful” minus “jobs hard to get” reaching the lowest level in January of this year and since the COVID pandemic recession, as shown in the graph below.

We were expecting these two effects, the tariff shock and the incentives for investing in capital, to diminish during the rest of this year and for employment to start improving, as we saw in the release of the January employment numbers. However, the Supreme Court’s decision on IEEPA, and the administration’s response, could throw another wrench into the economy’s path this year.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.